By Nkanu Egbe

Nigeria is running out of room.

Not in the physical sense, and not even in the way most people think about money. The country is approaching something far more dangerous—a point where its revenues can no longer sustain its obligations, where borrowing ceases to be a solution, and where even willing lenders begin to hesitate.

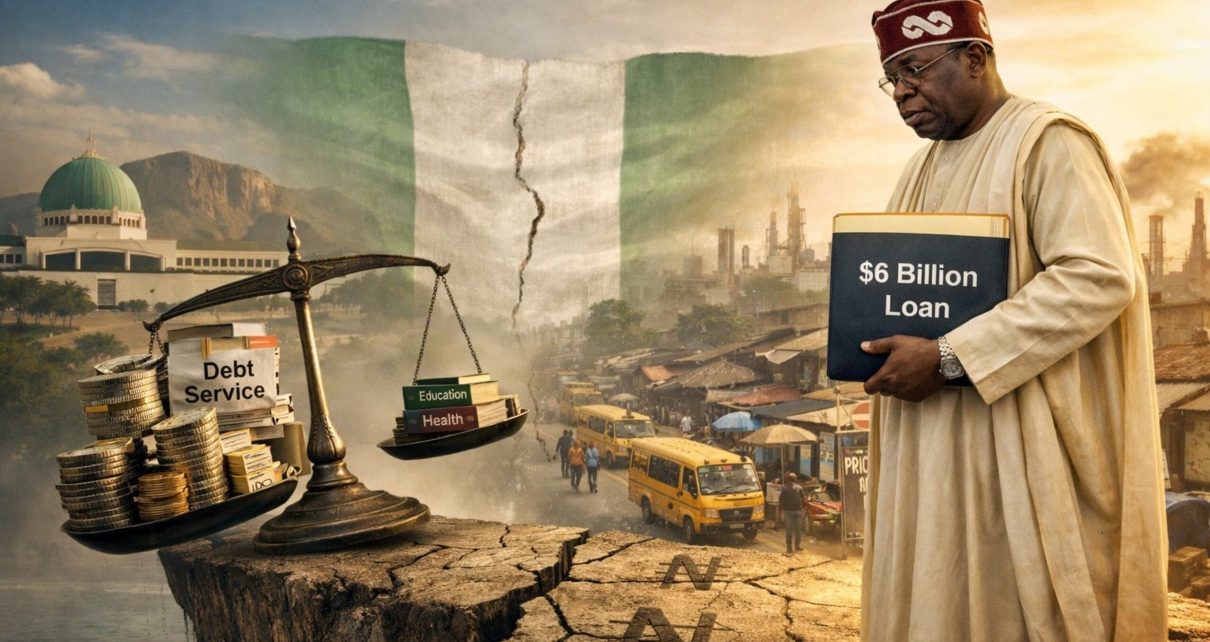

The $6 billion loan request sent by President Bola Ahmed Tinubu to the Senate in March 2026 is not just another routine financing move. It is a warning signal. Beneath the language of “bridge funding” lies a deeper truth: Nigeria is increasingly borrowing to survive, not to grow.

And unless something fundamental changes, the road ahead leads to a fiscal wall that may arrive as early as 2030.

Borrowing as Policy, Not Strategy

At the centre of the current fiscal debate is Nigeria’s 2026 budget, which carries a deficit of approximately ₦23.85 trillion. To plug that gap, the federal government has once again turned outward—seeking $5 billion from Abu Dhabi Bank and $1 billion from Citibank.

On paper, this is familiar territory. Governments borrow all the time. Infrastructure needs financing. Budget cycles require smoothing. Economic shocks demand intervention.

But there is a difference between borrowing as a tool and borrowing as a habit.

Nigeria is drifting into the latter.

The pattern has become predictable: deficits emerge, borrowing follows, and the underlying structure that produced the deficit remains largely untouched. What should be temporary intervention is gradually becoming permanent policy.

And that is where the risk begins to compound.

The Cost of Running the State

To understand the depth of the problem, one must look beyond the headline figures and examine how Nigeria spends its money.

The 2026 budget allocates roughly ₦15.25 trillion to recurrent non-debt expenditure. This is the cost of maintaining government—salaries, allowances, administrative overheads, and the sprawling network of ministries, departments, and agencies.

It is here that the imbalance becomes most visible.

Nigeria operates an expansive governance structure: an executive presidency, a bicameral legislature, and hundreds of federal agencies—many of which perform overlapping or duplicative functions. Over time, this structure has grown not strictly out of economic necessity, but out of political accommodation.

The result is a system that consumes a large share of national revenue simply to sustain itself.

The cost of governance, in effect, has become a first charge on the nation’s resources—before productivity, before investment, and increasingly, before development.

The Debt-Service Paradox

If the cost of governance defines how Nigeria spends, debt servicing defines its constraints.

In the 2026 fiscal framework, ₦15.52 trillion is allocated to servicing debt. That figure stands in stark contrast to the allocations for critical sectors:

- Education: ₦3.52 trillion

- Health: ₦2.48 trillion

Nigeria is spending nearly three times more on servicing debt than on the combined investment in education and healthcare.

This is more than a budgetary imbalance. It is a structural contradiction.

An economy cannot sustainably grow when it invests less in its people than it pays to its creditors. Human capital—education, health, skills—is the foundation of productivity. When that foundation is underfunded, growth potential weakens.

And when growth weakens, the ability to repay debt diminishes.

This is the paradox: the more Nigeria borrows under the current structure, the harder it becomes to escape the cycle of borrowing.

Oil, Collateral, and a Changing World

For decades, Nigeria’s fiscal model has rested on a single, powerful assumption—that oil revenues will continue to underwrite the nation’s finances.

That assumption is now under pressure.

The global energy landscape is shifting. Renewable energy adoption is accelerating. Climate policies are tightening. While oil remains important, its long-term dominance is no longer guaranteed.

For Nigeria, this introduces a critical vulnerability.

Oil is not just a source of revenue; it is also a signal to lenders. It represents future earning capacity. It underpins confidence.

As that confidence becomes less certain, so too does Nigeria’s ability to borrow on favourable terms.

The risk is not immediate collapse. It is gradual erosion.

And erosion, if unchecked, leads to structural failure.

The 2030 Fiscal Cliff

The concept of a “fiscal cliff” is often misunderstood. It does not mean that Nigeria will suddenly run out of money.

Rather, it describes a point at which revenue is no longer sufficient to sustain obligations—a point where borrowing becomes increasingly difficult, and where fiscal choices narrow dramatically.

If current trends persist, the trajectory is clear:

- Debt servicing continues to rise

- Recurrent expenditure remains high

- Oil revenues face long-term uncertainty

- Non-oil revenue growth lags behind needs

By 2028 to 2030, Nigeria could find itself in a position where even concessional lenders hesitate to extend further credit.

Not because Nigeria lacks potential—but because its fiscal structure signals risk.

At that point, the challenge is no longer about managing debt. It is about managing constraint.

Borrowing Without Transformation

Borrowing, in itself, is not the problem.

Many successful economies rely on debt to finance growth. The difference lies in how that debt is used.

When borrowing is tied to productive investment—roads, power, industry, education—it generates returns. It expands the economy. It increases revenue.

But when borrowing is used primarily to fund consumption—to pay salaries, maintain structures, and service existing debt—it does not create new value.

Nigeria’s current pattern leans heavily toward the latter.

This is the core of the sustainability problem.

Without a shift toward productivity-driven borrowing, each new loan adds pressure rather than relief.

The Quiet Erosion of Sovereignty

There is another dimension to this conversation, one that is less visible but equally important: economic sovereignty.

Every external loan carries conditions—explicit or implicit. It introduces obligations denominated in foreign currency. It exposes the economy to exchange rate risks.

As borrowing increases, policy flexibility narrows.

Decisions about spending, taxation, and monetary policy become increasingly influenced by external considerations—credit ratings, investor sentiment, repayment schedules.

Over time, this can lead to a subtle but significant shift: a nation’s economic choices are shaped not only by domestic priorities, but by the expectations of its creditors.

Nigeria is not there yet. But the trajectory warrants attention.

Why the System Persists

If the risks are so clear, why does the system continue?

Because it is easier to maintain than to reform.

Reducing the cost of governance requires confronting entrenched interests. Streamlining agencies affects jobs and influence. Restructuring legislative costs raises political sensitivities.

These are not merely technical decisions—they are political ones.

And so, incremental adjustments often take the place of structural change.

But incrementalism may no longer be sufficient.

What Must Change

Avoiding the fiscal cliff is not impossible. But it requires deliberate action.

First, the balance of spending must shift. Recurrent expenditure must be reduced, and capital investment prioritised.

Second, governance structures must be streamlined. Efficiency must replace duplication.

Third, revenue must be diversified. Nigeria cannot rely indefinitely on oil. Tax systems, exports, and private sector growth must be strengthened.

Finally, borrowing must be tied to productivity. Every loan must have a clear pathway to generating economic returns.

Without these changes, borrowing will remain a temporary fix to a permanent problem.

The Cost of Inaction

Behind every fiscal statistic lies a human reality.

When debt servicing crowds out investment in education, classrooms suffer. When healthcare is underfunded, lives are affected. When economic growth slows, opportunities shrink.

The fiscal conversation is not abstract. It is lived.

And the cost of inaction is cumulative.

A Warning, Not a Prediction

The $6 billion loan request is not, on its own, a crisis.

But it is a signal.

It tells a story of a system under strain—a system that is increasingly reliant on borrowing to sustain itself, and increasingly constrained in its ability to grow out of that dependence.

Nigeria still has time.

But time, like fiscal space, is not unlimited.

The warning signs are visible. The numbers are clear. The trajectory is known.

The question is whether the country will change course—

or continue on a path that leads, steadily and predictably, to the edge.

- Nkanu Egbe is an economist and Editor, Lagos Metropolitan

{kind=link}